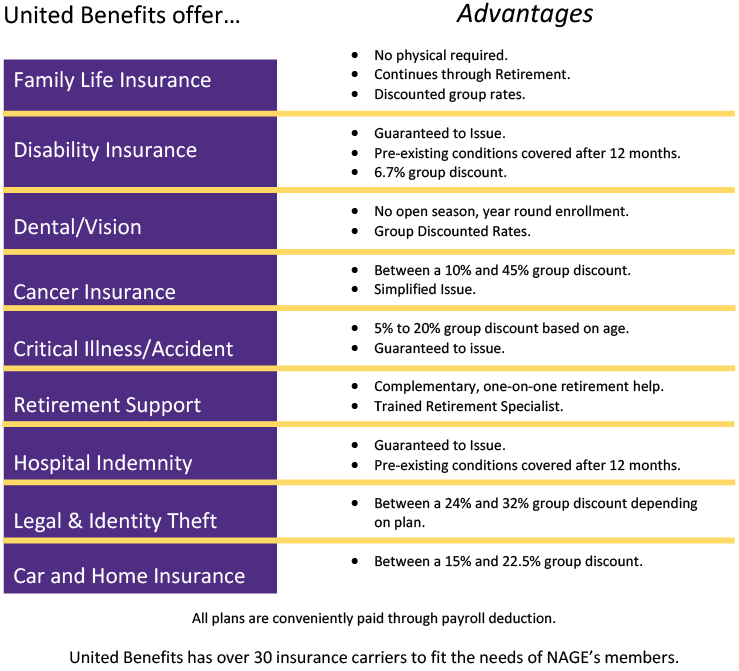

Life Insurance

There are benefits to buying the life insurance United Benefits designed for Union Members. Typically, when buying an individual life insurance policy, the premium and approval is determined by the insurance carrier’s underwriting requirements. They can perform a para-med exam which includes gathering information about the insured height, weight, blood pressure, urine sample, blood sample, etc. Along with answering extensive health questions the insurance carrier can also run a MIB script check, request medical records, check family history and/or run a MVR to complete the underwriting requirements. In result, many people are declined or must pay high premiums. We offer a couple different plans that are group discounted, guaranteed to issue, express issue, and/or simplified issue for Union Members. This way we can offer life insurance to those members who have never been able to buy in the past.

Examples:

• 5 Star life insurance company has a Term to age 100 plan that only has one knock out question which is if the client has HIV or AIDS. This plan is available for the member, spouse, children and grandchildren up to age 23. It also has great living benefits built into the plan depending on the state in which the member works.

• Mass Mutual is another Life Insurance carrier we offer that has a dividend paying Whole Life insurance plan and a Universal Life insurance plan. These two plans only have 3 simple health questions to qualify and have coverage available for the member, spouse, children, and grandchildren up to age 26.

• Combined/Chubb offers a Universal Life insurance plan to age 95 with only 3 simple health questions and have coverage available for the member, spouse, children and grandchildren up to age 17.

None of these plans require full underwriting to be approved because we have negotiated special underwriting for union members. We are also contracted with over 20 insurance carriers because we run into some members that have special life insurance needs. This way we can find the best rate for those members.

We also want to educate the members on their FEGLI, DC government life insurance, and/or group life insurance. For an example with FEGLI there is a basic, option A, B, and C the members are eligible to enroll in as a federal employee. Here are a few examples of how we educate members.

• The Basic is their salary rounded up plus 2,000. We encourage members to sign up for this plan because it is very inexpensive while they are working. However, at retirement the cost for the basic does increase and most of the time members are left with only 25% of their basic life insurance.

• The Option B, which is 1-5 times their base salary, is a 5-year renewable term. This means the cost increases as they get older and eventually becomes too expensive to keep. To offset the cost of Option B we have 10-, 20-, and 30-year term policies which can save members money. An employee with a $60,000 salary and 5 times their pay between ages 40 and 69 will spend $22,350 on their Option B. With a 30-year term the member can get the same coverage and save between $9,000 and $12,000.

• The Option C allows the employee to get a maximum coverage amount of $25,000 on their spouse and $12,500 on their children. What most employees do not realizes is their children’s life insurance policy drops off at age 23. Through our plans the children’s coverage will continue if the policy is being paid. There are also higher coverage amount options for the spouse and children depending on plan.

Voluntary insurance plans

There are many voluntary insurance plans one can enroll in as a government employee or as an individual. However, getting approved for these benefits differ from the plans United Benefits offer to union members. Most voluntary insurance plans are fully underwritten, which means they can require the proposed insured to answer health questions, run a MIB script check, check medical history, check family history, and/or check credit history just to name a few. These plans can also be rated based on the underwriting requirements as well as the employees’ age and occupation at the time of enrollment. Another significant difference is our plans cover pre-existing conditions after 12 months, whereas most plans exclude any pre-existing conditions or decline the insured because of them. The voluntary insurance United Benefits offers is either guaranteed to issue and/or simplified issue. We have listed these products below and the details on each one.

• Short Term Disability is a great plan for some federal employees because most government agencies do not offer this type of benefit. Through our disability plan the members get a guaranteed to issue policy up to a $3000 per month benefit if they have been actively working for 30 days and work at least 27 hours a week. Our base plan offers a 14-day elimination period with a 1-year benefit covering an accident or sickness on and off the job. This plan pays in addition to any sick or annual leave and the benefit is tax free, with coverage on pre-existing conditions after 12 months and covers maternity/pregnancy as a sickness. An example of the savings union members get if they qualified for a $3000 per month benefit plan is between $137.02 and $986.57 per year.

• Hospital Indemnity is designed to help offset the cost for hospital confinement by paying members a benefit directly to them. This plan is also guaranteed to issue if the member has been actively working for at least 30 days and works at least 27 hours a week. It also covers pre-existing conditions after 12 months and covers maternity/pregnancy as a sickness.

• Our Cancer Care Plus plan is a comprehensive cancer plan that also covers dreaded diseases. The best thing about this plan is our group discounted rate. For example, if one was to buy this as a non-union member, they would pay an individual rate instead of the group rate. The savings is between $42 and $200 per year for employee only coverage and $189 and $446 per year for family coverage depending on the age at enrollment.

• We offer AFLAC Accident and Critical Illness on a group rate. The best thing about these plans is they are guaranteed to issue. We have members who have tried to get these plans directly from AFLAC and have been turned down. Through us they were approved. The Aflac plan discount varies by state.

• Legal Shield is a group discounted service which includes prepaid legal and identity theft protection. The total savings for purchasing the services through United Benefits is $8.01 per month for individual and $16.00 per month for family.

United Benefits Retirement Plans

United Benefits provides its services without a fee to members or the organization. We teach lunch and learns and workshops on many topics that include but not limited to CSRS, FERS, FERS Supplement, special provision such as LEO, Social Security, TSP, 401a, 457b, FEHB, Medicare, IRA’s and spousal options to mention a few topics. We then provide free one on one counseling to assist the members on their specific needs and calculations of their retirement and deductions from such.

• Federal example: We calculate the FERS or CSRS. Break down the deductions on the post retirement options. We register them if not previously with Social Security.gov and explain social security options. We then go over their TSP (thrift savings plan) and the pre and post retirement options. We discuss a retirement budget and help show them options on how to get to their goal.

As a complementary benefit, United Benefits will assist any member in completing their application for retirement. This seems to be a popular benefit as members do not understand their multi-tier retirement system. Under the current agency budgets members do not have local agency help with understanding their retirement system. For the current members to understand the full picture they would need to contact OPM/HR department for the FERS/CSRS portion. Then contact TSP for assistance with the tsp options. Then lastly contact Social Security administration to understand their Social Security options. Even contacting each agency, the agencies do not do a good job of explaining the member’s options and strategies. The other problem is the terminology curve for the members to understand. We pull it together for the members so they can look at the larger picture and understand their options. Many members we meet with have made incorrect and costly decisions due to the lack of knowledge.